Why the Bank of Canada Might Cut Its Policy Rate to 1.75%

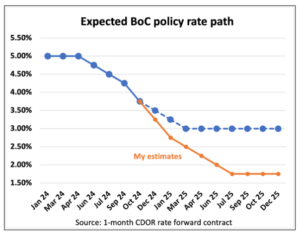

The Bank of Canada (BoC) may be forced to lower its policy rate more than anticipated, extending its current easing cycle into the second half of 2025. According to Ben Rabidoux of Edge Realty Analytics, the central bank could reduce its policy rate to 1.75% by July 2025 due to worrying economic trends.

Key Factors Behind the Predicted Rate Cut

Rabidoux’s prediction stems from a variety of economic indicators, including a declining per capita GDP and potential negative population growth due to federal immigration cuts. These factors, he believes, will put downward pressure on the economy, making further rate cuts inevitable.

The Impact of a 1.75% Policy Rate on Canadians

If the BoC follows through with a 1.75% policy rate by mid-2025, it would lead to a reduction in the prime rate to 3.95%. This, in turn, would lower interest rates on variable-rate mortgages, personal loans, and home equity lines of credit by as much as 200 basis points, benefiting many borrowers.

Source: edgeanalytics.ca

Current Market Predictions for the Bank of Canada’s Rate Decisions

While Rabidoux believes the market has underestimated the need for further rate cuts, many analysts predict a more gradual easing cycle. Current market expectations point to a 50-basis-point cut in December, with further reductions bringing the BoC’s rate to around 3% by mid-2024.

Canada’s Slowing Economy and Declining GDP

A key driver behind the rate cut prediction is Canada’s slowing economic growth. Per capita GDP has been declining for the past two years, and Rabidoux warns that the country is at risk of a slight economic contraction. The federal government’s recent decision to scale back immigration could exacerbate this slowdown, as population growth has been a significant contributor to Canada’s GDP growth.

The Looming Mortgage Renewal Crisis

One of the most pressing concerns for the Bank of Canada is the wave of mortgage renewals expected in 2025 and 2026. Many borrowers who locked in low interest rates during the pandemic are now facing the prospect of significantly higher payments. Rabidoux argues that in order to avoid a “payment shock,” the BoC must reduce its rates further.

Canada’s Resilience Amid Record-High Interest Rates

Despite the challenges posed by high interest rates, Canadians have remained relatively resilient. Mortgage arrears and insolvencies remain low by historical standards. However, the Canada Mortgage and Housing Corporation (CMHC) has warned that mortgage arrears in major cities like Toronto and Vancouver could rise to decade-high levels over the next 6 to 12 months.

Concerns About Business Insolvencies and Job Losses

While mortgage borrowers have held up well, the business sector is showing signs of distress. Business insolvencies have been rising, and Rabidoux notes that this could soon lead to job cuts, impacting the broader labor market.

Inflation and the Bank of Canada’s Room to Act

Rabidoux believes that as long as inflation remains within the Bank of Canada’s target range—and with signs that rent and mortgage interest costs are cooling—the BoC will have the flexibility to continue easing. This could include reducing the policy rate by another 200 basis points by mid-2025.

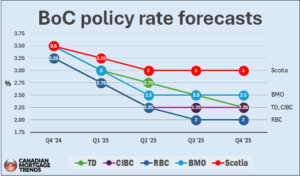

Big Banks Predict More Modest Rate Cuts

While Rabidoux’s forecast is more aggressive than most, some of Canada’s biggest banks share the outlook of rate cuts, though they expect them to be less dramatic. RBC, for example, forecasts that the BoC’s policy rate will drop to 2.00% by the third quarter of 2024, while Scotiabank predicts the central bank will cut rates by 75 basis points before holding steady at 3.00%.